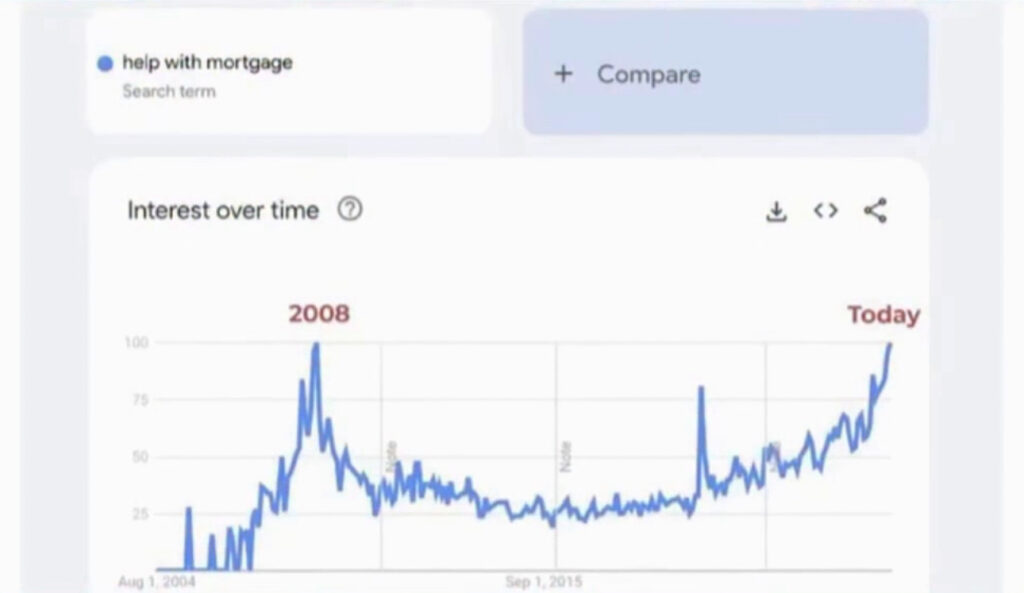

Prospective homebuyers scrolling through property listings this spring confront a question that transcends usual affordability calculations: whether current market conditions resemble the calm before 2008’s catastrophic storm, or merely represent cyclical difficulties that disciplined buyers can navigate successfully. The answer emerging from converging data streams suggests caution bordering on alarm—Google searches for “help with mortgage” have reached frequencies last recorded when the global financial system teetered toward collapse, whilst concrete UK market indicators show fundamentals deteriorating in ways that transform property purchase from wealth-building strategy into potential financial trap.

Average UK house prices fell 0.5 percent in March to £299,677 according to Halifax, reversing February’s modest gains as lenders executed the largest single-day withdrawal of mortgage products since Liz Truss’s disastrous mini-Budget triggered market panic in 2022. Hundreds of the cheapest lending deals vanished overnight, leaving prospective buyers facing dramatically narrowed options at substantially elevated rates—a combination that financial historians recognise as precursor to broader market dysfunction rather than routine volatility.

The search data alone might warrant dismissal as digital anxiety divorced from underlying reality. Yet when homeowners’ desperate queries for mortgage assistance coincide with actual product disappearance, falling prices, and inflation dynamics that prevent interest rate relief, the pattern suggests not irrational panic but rational response to genuinely deteriorating conditions. Amanda Bryden, head of mortgages at Halifax, confirmed the causation: “Concerns about higher energy prices have pushed up inflation expectations, which in turn led to a rise in mortgage rates, reducing confidence that interest rates will be cut this year and dampening the initial momentum in the market.”

For anyone contemplating property purchase in this environment, the strategic question becomes whether to proceed despite warning signals, defer until conditions clarify, or abandon homeownership ambitions entirely in favour of preserving capital flexibility. Each choice carries profound implications for decade-long financial trajectories.

What Makes This Moment Uniquely Treacherous for New Buyers

First-time buyers and those stretching finances to upgrade face vulnerabilities absent from established homeowners’ calculations. Existing mortgage holders locked into fixed rates below 6 percent possess buffer against payment shock, whilst many accumulated substantial equity during recent appreciation that provides cushion against price declines. New entrants enjoy neither protection—they purchase at elevated prices using expensive debt whilst market fundamentals deteriorate beneath them.

UK Finance forecasts just 2 percent growth in purchase lending for 2026 following 2025’s 22 percent surge, with 10,000 fewer property transactions projected as affordability pressures intensify. This deceleration reflects not absence of demand but systematic exclusion of marginal buyers whose income-to-price ratios no longer satisfy lender requirements at current rates. Those who barely qualify today may discover themselves unable to refinance when initial fixed periods expire, facing payment increases they cannot afford whilst trapped in properties they cannot profitably sell.

The Iran war’s energy price legacy compounds these structural challenges. Oil remains 30 percent more expensive than pre-conflict levels despite Wednesday’s conditional ceasefire driving Brent crude down 15 percent to $94 per barrel—a commodity shock that feeds directly into inflation calculations governing Bank of England interest rate decisions. UK inflation stood at 3 percent in February, above the central bank’s 2 percent target, before March’s additional energy cost increases. Petrol and diesel prices reached highest levels since late 2022 according to RAC data, ensuring sustained upward pressure on headline inflation metrics.

This creates perverse timing for property purchase: the same energy shocks straining household budgets through higher transport and heating costs simultaneously prevent the interest rate cuts that might make mortgages more affordable. The Bank of England had “hinted at cutting interest rates this year,” offering hope that borrowing costs might ease. Those hints now appear premature, with market participants pricing minimal probability of cuts whilst concrete risk of additional increases emerges if inflation accelerates further.

Buyers entering the market today therefore face worst of both conditions—elevated purchase prices reflecting years of appreciation combined with high borrowing costs likely to persist longer than anticipated. The traditional calculus that property ownership builds wealth assumes either stable prices with manageable debt service, or rising prices offsetting expensive financing. Current conditions offer neither assurance.

Why Geographic and Sector Variations Matter for Individual Risk Assessment

The aggregate statistics obscure crucial regional and property-type variations that determine whether specific purchases represent acceptable risk or financial recklessness. California’s pronounced spike in mortgage help searches reflects one of America’s most expensive housing markets where high property prices, insurance costs and property taxes create vulnerability even among employed professionals. Similar dynamics affect London and southern England, where property-to-income ratios stretch affordability to breaking points that leave minimal margin for additional shocks.

Conversely, northern England and Scotland demonstrate more favourable buying-versus-renting calculations according to regional analyses, suggesting that blanket warnings against property purchase ignore meaningful geographic heterogeneity. A buyer in Newcastle facing property costs at reasonable multiples of local wages confronts fundamentally different risk profile than London equivalent stretching to seven or eight times income for marginal accommodation.

Property type similarly influences vulnerability. New-build purchases in oversupplied developments face dual risk of construction quality issues and price depreciation as developers compete for shrinking buyer pools. Established properties in supply-constrained areas with strong employment bases offer relative security, though no immunity from broader market corrections.

The buy-to-let sector faces particularly acute pressures. New landlord purchase lending grew 11 percent in 2025 to £11 billion but UK Finance forecasts zero growth in 2026, constrained by additional taxes, enhanced regulation, and yields insufficient to compensate for higher borrowing costs. Prospective landlords contemplating property investment confront not temporary headwinds but structural shifts rendering traditional models uneconomic.

Climate vulnerability introduces additional dimension that David Burr—whose prediction of 2008’s crisis earned him profile in “The Big Short”—identifies as emerging threat. Properties in flood-prone areas or coastal zones face insurance cost increases that create payment stress independent of mortgage rates, potentially rendering homes unsaleable when buyers cannot secure affordable coverage. This risk concentrates geographically, making property location assessment critical beyond traditional transport links and school quality considerations.

The Case for Deferral Versus the Cost of Waiting

The argument for postponing purchase rests on multiple foundations. Falling prices suggest better value awaits those who preserve capital and flexibility—March’s 0.5 percent decline may prove initial movement in larger correction as stretched affordability meets deteriorating economic conditions. Mortgage product withdrawal indicates lender pessimism about market direction, with financial institutions possessing superior data and analytical resources concluding that risk no longer justifies lending at previous rates or terms.

The 1.8 million UK homeowners whose fixed-rate deals expire in 2026 will flood refinancing markets seeking new terms, potentially overwhelming lender capacity and forcing additional rate increases or product restrictions. New buyers entering simultaneously would compete for limited lending allocation whilst established borrowers exercise priority claims on lender relationships.

Deferred purchase preserves optionality. If conditions stabilise and prices resume appreciation, the buyer re-enters having sacrificed some upside but avoided downside risk. If conditions deteriorate into genuine crisis, the deferral prevents catastrophic loss—the difference between renting through correction versus owning whilst equity evaporates and negative equity traps emerge.

Yet deferral carries costs beyond foregone appreciation. Rental payments represent pure consumption without equity accumulation, whilst continued saving for deposits faces erosion from inflation that may exceed interest earned on savings accounts. The psychological burden of indefinite delay—watching friends and family achieve homeownership whilst remaining tenant—imposes stress that economic models struggle to quantify but individuals feel acutely.

More fundamentally, perfect market timing proves impossible. Those who deferred purchase in 2019 hoping for better opportunities instead watched prices surge during pandemic whilst mortgage rates remained historically low—missing window that may not reopen for decades. The prospective buyer faces not choice between good and bad timing but between imperfect present and uncertain future.

James Tatch at UK Finance acknowledged this tension: “The mortgage market showed strength in 2025, particularly for house purchases. But even with welcome tweaks to lending regulations this year, affordability is now very tight and this is likely to limit borrowing options for potential buyers in 2026.” The phrasing suggests market remains functional whilst acknowledging constraints—hardly ringing endorsement but neither outright warning to avoid purchase entirely.

What Disciplined Buyers Can Still Achieve Despite Headwinds

For those proceeding with property purchase despite warning signals, risk mitigation becomes paramount. Maximum deposit percentages reduce loan-to-value ratios, providing equity cushion against price declines whilst securing better interest rates and avoiding higher-LTV premium pricing. Buyers stretching to minimal deposits sacrifice both buffers, amplifying vulnerability to market movements.

Conservative income assessment matters equally. Lenders calculate affordability using stress tests that assume rate increases, but individual buyers should apply even stricter personal standards—budgeting for payments at rates two or three percentage points above current offers ensures capacity to refinance even if conditions deteriorate. Those whose affordability depends on current rates continuing have purchased risk they cannot manage.

Fixed-rate term selection involves tradeoffs between certainty and cost. Longer fixes—five or even ten years—provide extended payment predictability at premium pricing, whilst shorter two-year deals offer lower initial rates but expose borrowers to refinancing risk when terms expire. Current uncertainty argues for longer fixes despite cost, trading expense for security that market conditions in 2028 or 2030 won’t force unaffordable refinancing.

Property selection should prioritise liquidity over perfect specification. Homes in strong employment centres with good transport links and school catchments maintain demand through market cycles, whilst specialist properties—period conversions, architectural statements, homes requiring extensive renovation—appeal to narrower buyer pools and prove harder to sell during downturns. The boring suburban semi offers better crisis resilience than the characterful rural barn conversion.

Critical employment stability assessment precedes any purchase decision. Buyers in secure professions with portable skills—healthcare, education, core financial services—face different risk profiles than those in cyclical industries vulnerable to economic slowdowns. The mortgage that seems manageable with current employment becomes catastrophic when redundancy arrives and replacement income proves elusive.

Mortgage Bankers Association data showing delinquency rates rising from 0.15 to 0.20 percent of all loans, whilst still historically low, demonstrates that some borrowers already experience stress. These early casualties likely include those who stretched furthest, saved least, or faced employment disruption—mistakes future buyers should study rather than replicate.

The philosophical question underpinning purchase decisions asks whether homeownership remains appropriate goal in unstable conditions, or whether flexibility and capital preservation better serve long-term wealth building. Traditional wisdom holds that property ownership anchors family stability and forces disciplined saving through mortgage repayment. Yet that wisdom emerged from eras of reliable appreciation and affordable debt—conditions no longer assured.

Renting preserves mobility to pursue employment opportunities without property sale constraints, avoids maintenance costs and property tax burdens, and prevents capital lock-in that reduces ability to pursue alternative investments. For young professionals in career-building phases, these advantages may outweigh homeownership’s benefits—particularly when purchase would require geographic commitment to uncertain employment markets.

The search data’s message proves unambiguous: millions of existing homeowners experience sufficient mortgage stress to seek help online at frequencies matching the worst financial crisis in generations. Whether that stress crystallises into mass defaults or remains contained within manageable parameters depends on factors still unfolding—inflation trajectories, employment stability, energy prices, central bank responses, and geopolitical developments beyond individual control.

Prospective buyers must therefore assess not whether current conditions seem ideal—they manifestly do not—but whether personal circumstances permit managing downside scenarios if conditions deteriorate further. Those with secure employment, substantial deposits, conservative income calculations, and flexible life circumstances may reasonably proceed despite headwinds. Those lacking these advantages should recognise that property purchase in deteriorating markets has historically produced catastrophic outcomes for marginal buyers who discover too late they purchased beyond their capacity to withstand adversity.

The 2008 crisis taught that markets can deteriorate faster and further than optimists imagine, that lender confidence can evaporate overnight, and that individual financial ruin often begins with decisions that seemed reasonable given information available at the time. Today’s information—search desperation matching crisis levels, falling prices, product withdrawal, inflation persistence, geopolitical instability—suggests conditions warrant extreme caution rather than confidence that “it’s always a good time to buy.” Sometimes the wisest property decision involves recognising when not to buy at all.